MapX: Manage Your Assets, Properties and Map It For Visualization

Technology for Real Property Mapping and Assessment at Your Fingertips

MapX is a complete real property mapping and assessment solution that uses advanced geoinformatics technologies. Our company is a product of innovation and extensive research in spatial mapping, and visualization and interactivity for high-end mapping services. We endeavor to improve efficiency in the current process of administering real property tax mapping by harnessing the power of modern technologies.

Today, we bring you MapX! Your convenient and hassle-free real property solution made available at the tips your hand.

A technical description is a document consisting of a plan and a report which describes the property with regards to cadastral limits and for specific purposes such as the right of way, draining servitude, encroachment servitude, agricultural zoning, annexation, sale or municipal fusion. MapX uses artificial intelligence (AI) technology to capture details and descriptions on a given map. The use of this advanced technology proves faster and accurate in plotting map figures compared to traditional manual map plotting.

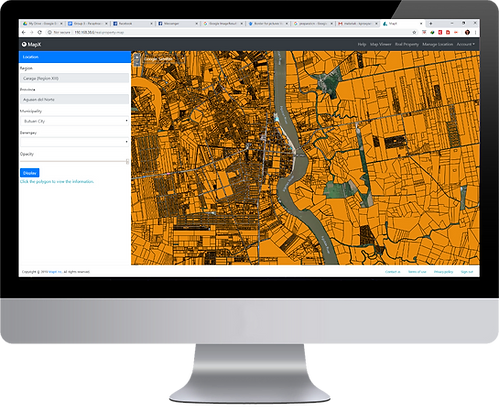

Parcellary Mapping is an interactive webGIS features of MapX where users are empowered to plot survey plans and lot data computation from cadastral maps into the portal. Plotting of boundaries are based from the metes and bounds described in the survey plan.

Tax map sectioning is mandated to be done every three years to accommodate changes in parcellary boundaries for each classified area in the locality. Map generations using the prescribed numbering convention set by the Bureau of Local Government Finance (BLGF) will be automatically generated by the portal.

MapX employs data mining technology to come up with the latest and updated fair market value of the property.

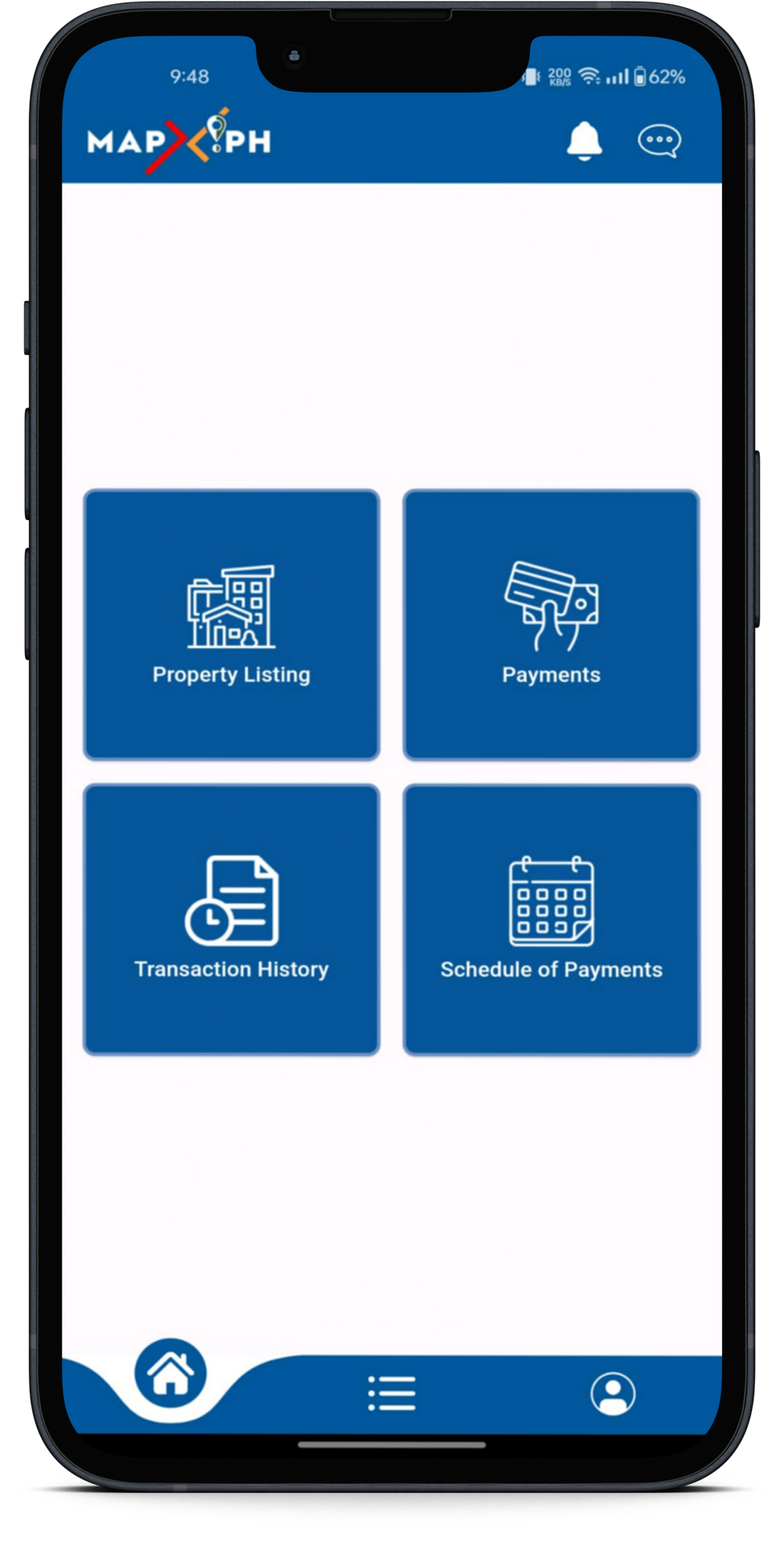

Payment Feature

Experience seamless transactions with our mobile app's integrated payment feature.

Property Listing

Worried having more than one land asset? We got you covered. Our mobile app enables the user to list and tag the location of its assets for easier and faster tax mapping.

Real-Time Notification

Receive timely notifications and reminders to track and manage your property tax obligations with ease.